Maybank Dominates Digital Banking With 10.68M Active Users

Malaysia-based Maybank maintained its leadership in digital banking while posting steady financial results for the nine months ended September 2025, demonstrating resilience across its regional operations.

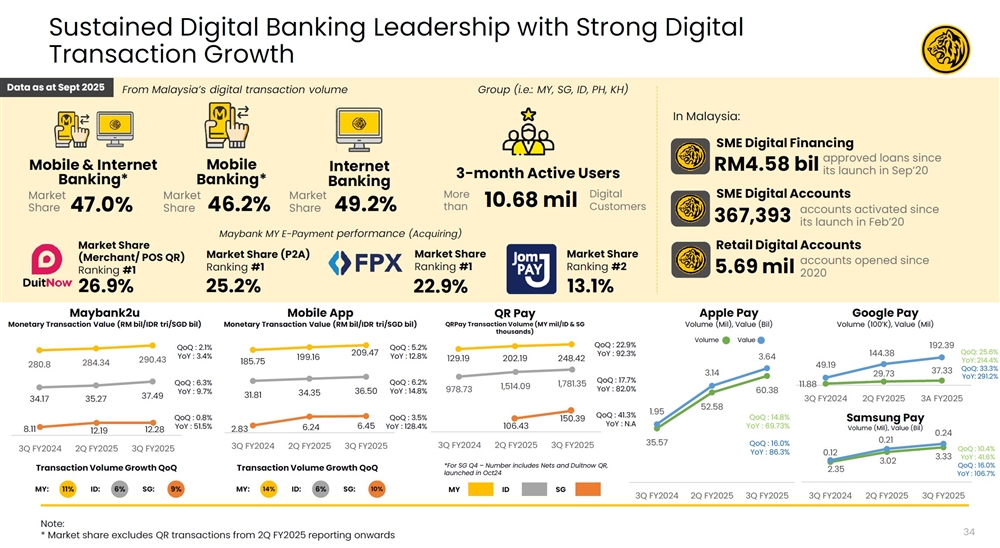

The bank commands a 46.2 percent market share in mobile banking transactions and 49.2 percent in internet banking transactions in Malaysia, underscoring its dominance in digital financial services. The digital platform serves 10.68 million active users monthly, with 5.69 million retail digital accounts opened since 2020.

In market positioning, Maybank holds 19.6 percent of consumer loans in Malaysia, including 28.9 percent of auto retail hire purchase and 16.6 percent of mortgage financing. The bank commands 21.3 percent of the credit card receivables market and maintains 24.5 percent market share in retail current account and savings account deposits.

Digital transaction volumes expanded significantly during the third quarter of 2025. Mobile app monetary transactions reached RM209.47 billion for Malaysia, alongside growth in Indonesia and Singapore operations. QR payment transaction volumes grew 14 percent quarter-on-quarter in Malaysia, reaching 248.42 million transactions.

For the nine-month period, Maybank reported net profit of RM7.84 billion, up 3.7 percent from the previous year. This was supported by net operating income of RM22.86 billion, which increased 3.2 percent year-on-year. Net fund-based income rose 1.6 percent to RM14.90 billion, while non-interest income climbed 6.3 percent to RM7.96 billion.

Net interest margin for the nine months stood at 2.03 percent, down one basis point from a year earlier. However, the bank improved its third quarter net interest margin to 2.02 percent, up two basis points from the previous quarter through proactive liquidity and funding cost management.

Overhead expenses increased 3.8 percent to RM11.18 billion, reflecting strategic investments for long-term growth and inflationary adjustments in personnel expenses, marketing costs and IT expenditure. The cost-to-income ratio remained stable at 48.9 percent, contributing to a 2.7 percent rise in pre-provisioning operating profit to RM11.68 billion.

Net impairment provisions eased to RM1.25 billion, improving 1.5 percent year-on-year following the completion of a corporate borrower restructuring exercise and recoveries in the non-retail portfolio. The net credit charge-off rate improved to 11 basis points from 26 basis points in the same period last year.

Asset quality metrics showed a gross impaired loans ratio of 1.32 percent compared to 1.26 percent previously, while loan loss coverage remained at 110.1 percent.

The loan book expanded 2.7 percent year-on-year to RM681.7 billion as at September 2025, led by Malaysia which increased 6.0 percent to RM435.2 billion. Singapore loans rose 1.5 percent, while Indonesia declined 0.5 percent as the unit rebalanced its corporate lending portfolio.

Deposits grew solidly to RM739.1 billion from RM706.2 billion a year earlier. Current account and savings account balances improved to RM295.0 billion, marking a 15.2 percent year-on-year increase. Fixed deposits rose 4.1 percent to RM358.9 billion.

Capital positions remained robust with the CET1 capital ratio at 14.9 percent and total capital ratio at 19.3 percent. The liquidity coverage ratio stood at 141.2 percent, above the regulatory requirement of 100 percent.

Wealth fees increased 23.5 percent year-on-year to RM1.07 billion, while foreign exchange sales income for wealth and small-medium enterprise segments rose 2.9 percent and 8.7 percent respectively. Non-retail loan growth recorded increases of 8.1 percent, 10.9 percent and 9.6 percent across Malaysia, Indonesia and Singapore.

For the insurance and takaful business, underwriting income reached RM840.55 million, up 23.7 percent from the previous year driven by the family takaful portfolio. Profit before tax declined to RM941.17 million from RM1.01 billion previously due to softer equity market conditions and unfavorable yield curve movements. The group maintained the top position in general insurance and takaful in Malaysia with 16.7 percent market share, and fourth place in life and family new business with 11.6 percent market share.